Overfitting is not one bug. It is usually a stack of subtle mistakes that jointly inflate historical performance and collapse out-of-sample behavior.

The Seven High-Impact Traps

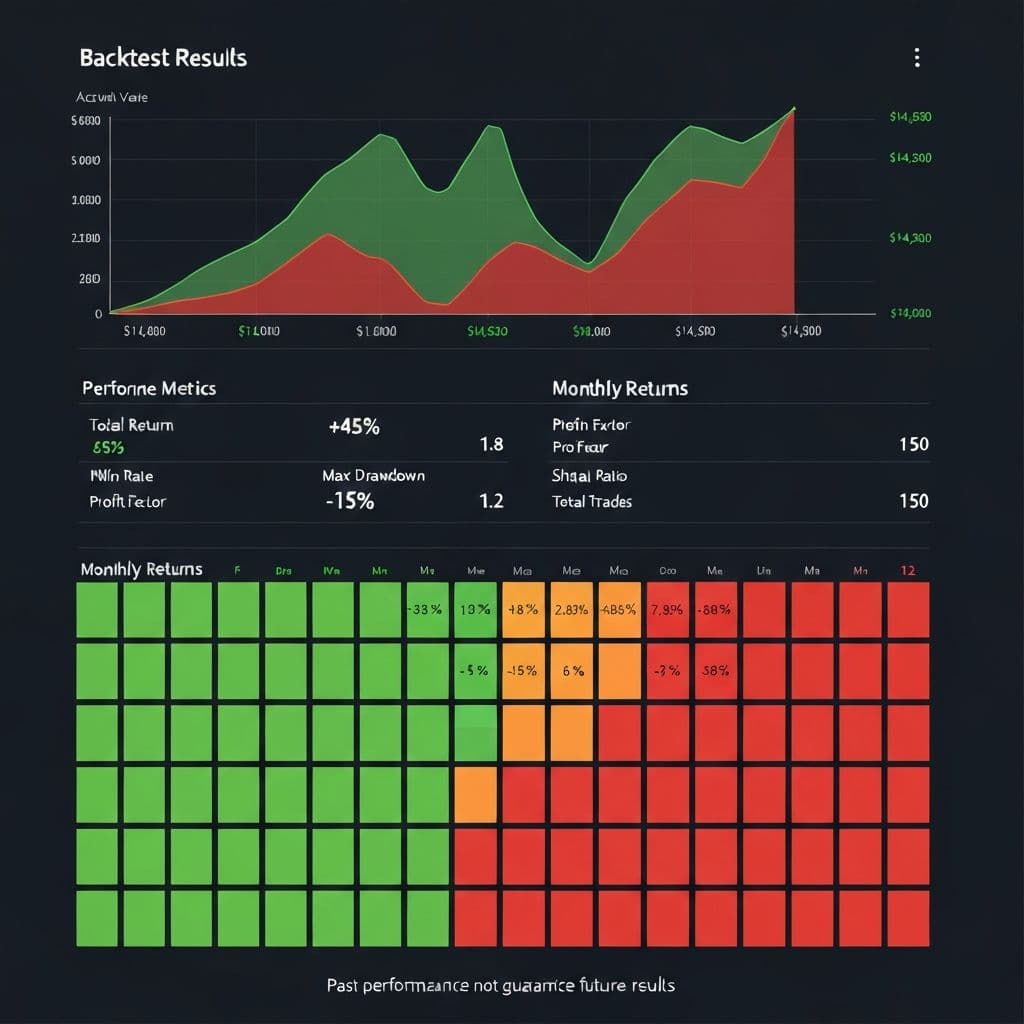

QuantumEdge

Explore these ideas in live bot templates

See how this setup translates into production-ready workflows.

Browse QuantumEdge bot templates- Look-ahead bias in indicators or feature joins.

- Survivorship bias in symbol universe selection.

- Data snooping from repeated parameter mining.

- Ignoring realistic fees, spreads, and slippage.

- Training and validating on overlapping windows only.

- Using unstable objectives like raw CAGR alone.

- Skipping stress tests for low-liquidity conditions.

A Better Validation Workflow

- Use walk-forward splits with strict time ordering.

- Track parameter stability across adjacent regions.

- Require edge persistence across multiple market regimes.

- Stress with spread widening and delayed fills.

The goal is not to find the single best backtest line. The goal is to find behaviors that remain acceptable after uncertainty, friction, and regime change are applied.